Nassim Taleb, and Benoit Mandelbrot before him, referred to “black swans” as extremely rare, significant events with non-calculable probabilities. Covid-19 is not such an event and its consequences are quite predictable. Among other things, Covid-19 may have accelerated the dominant trends in the economy, with significant impact on long-term expected returns of equities and bonds.

There is a school of thought that our experience of Covid-19 is largely due to the echo chamber created by social media. If this were the case, it is hard to imagine that the global pandemic could have any meaningful long-term impact on the economy. To a very limited extent this line of reasoning is justified; there are many things about the novel corona virus that are very unremarkable: we have experienced viruses both deadlier and more contagious, even viruses that are deadly and contagious at the same time.

- Detailed assessment of pandemics in the last 1000 years and why this history is NOT applicable

- Detailed industry-by-industry assessment and impacts

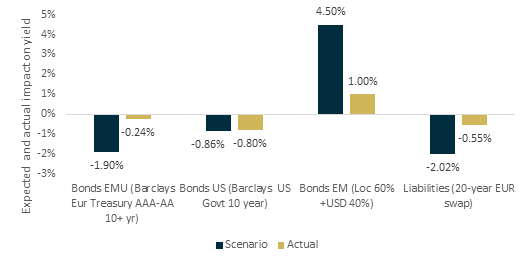

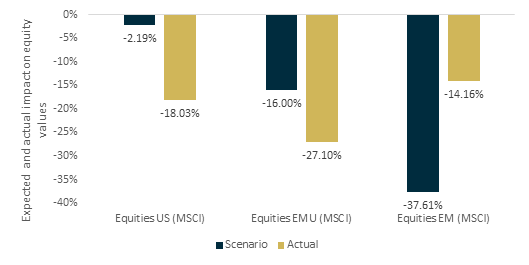

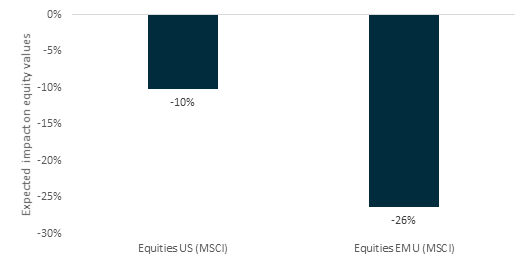

- Relevant impacts for interest rates, equities, GDP and profitability by region

- Calculations based on the comprehensive data-driven forward looking Mira ABM analysis

Precisely because of this, Covid-19 is not a “black swan” event in the sense that almost all its features are very ordinary. In fact, the novel corona virus is remarkably like another very average virus – the one that caused the 1918 flu pandemic killing by some estimates nearly 100 million people and causing multiple decades of economic impact.

Webinar / Covid-19: The Long-term Impact

Full webinar is now available. Click below to access the recording.