Earlier China nCoV Scenario

On February 6, 2020, urged by our clients, we introduced a stress scenario in Mira ABM called China-2019 nCoV to reflect the quickly spreading epidemic of a yet unnamed disease in China. At the time our concerns were:

- China will in lock-down for up to three months, with the economy working only at the quarter of capacity

- Intra-Asian traffic will slow down for one quarter

- Although in retrospect, these assumptions appear to be mild now, at the time this was perceived to be the severe and plausible case. Mira ABM assessment showed a significant risk to equities and much lower yields.

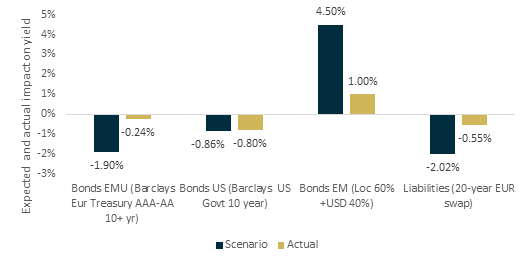

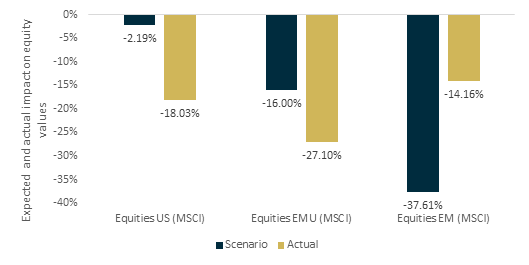

This scenario was broadly in line with what happened at first. Asian air traffic did collapse and China appears to have been shut for business for 3 months now. The resulting performance was broadly in-line with the forecasts, although it appears that Mira ABM underestimates the performance of US equities and overestimates moves in EU Bonds/interest rates – an area we will focus our research on.

The New Scenario

The subsequent events, however, require a reassessment and introduction of a new scenario that is only nominally triggered by the Covid-19 disease. The scenario reflects:

- Sharply lower oil price environment,

- Lower global demand for travel,

- Sudden freezing of commercial aircraft orders from Boeing and Airbus

Lower oil prices, triggered by slowing demand due to Covid-19 triggering a slow-down in transport traffic, has resulted in a global price war. Our assumptions are that countries with lower cost of production will continue to sell at current prices, so will see higher volumes, while countries with higher cost of production (e.g. US shale oil), will face declining volumes as well as prices.

Rapidly falling airline traffic has placed most airlines dangerously close to insolvency. IATA have recently published their limited spread and extensive spread scenarios, that estimate global airline industry loss of revenue at 11% and 19% respectively.

| Revenue | Volume | |

|---|---|---|

| Limited spread |

11% | 10% |

| Extensive spread |

19% | 15% |

What IATA does not take into account (in fact notes to the contrary) is that far from being positive for airlines, lower oil prices actually create a huge immediate pressure due to oil price hedges. Any benefit from low oil price would be accrued during the year, as and when the airlines operate and sell tickets, while the losses from hedging position are immediate. If the travel volumes drop drastically, so does any benefit from low oil prices, while the losses on hedging position remains.

Finally, aircraft manufactures (Boeing and Airbus) see abrupt market halt of historical proportions. In February, both companies experienced ZERO new orders, which has not been the case in decades.

| Industry | Price | Volume |

|---|---|---|

| Airlines globally | -15% | -25% |

| Aircraft manufacturers | -10% | -10% |

| Russian oil | -30% | -5% |

| US oil | -30% | -20% |

| Rest of world oil | -30% | 10% |

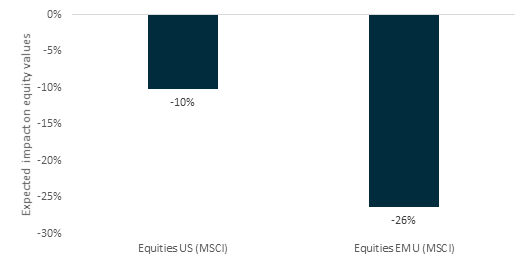

At the time of publication of this article, Mira ABM users are able to assess the impact of this new scenario on their portfolios. Impact on equities, given LINKS Default World View, are in the range of 10-26%, while impact on yields are 150 basis points.