Contradictory macro- and microeconomic observations in today’s economy are a norm, and the recent earnings season in the U.S. only adds to the uncertainty. Unfortunately, wishful thinking is not a way out this time either: putting the pieces of puzzle together reveals the state of economy that is not new.

One of the biggest challenges of having a consistent asset return framework is trying to reconcile the assumptions, inputs and returns with the myriad of macro- and microeconomic observations. Often contradictory observations peacefully coexist in the global economy, raising alarms and questions. In this issue of Risk Wire we have tried to take an inventory of key observations (contradictory or not) and tie them together in the context of the Graham Risk framework.

The first observation – the actions of the Central Banks, are clearly the focus of the investment community, with ECB, the Fed and BoE extending unconventional policies. Acronyms like ZIRP and NIRP have become the favourite in the community, as many veteran investors have launched critical attacks of the central bankers. One of the most unrestrained attacks by Bill Gross appeared in an article on October 5, 2016:

“Central bankers have fostered a casino like atmosphere where savers/investors are presented with a Hobson’s Choice, or perhaps a more damaging Sophie’s Choice of participating (or not) in markets previously beyond prior imagination. Investors/savers are now scrappin’ like mongrel dogs for tidbits of return at the zero bound. This cannot end well.”

The second observation, which is hard to reconcile with the first one, is the strong earnings season in the third quarter of this year. Although the season is not over yet, so far a double-digit recovery in earnings is at hand, which is the first positive sign since the late 2014 that corporate America is back to health. Our third observation – higher oil and other main commodity prices can be easily reconciled with stronger earnings season, and with stronger labour market – the fourth observation.

All of the above, however, cannot coexist in an environment of overcapacity in most industries, falling prices for agricultural commodities and the generally deflationary environment. The cocktail of these observations is so inconsistent that a “deeper dive” is warranted in multiple asset categories, geographies and sectors to untangle the web of dependencies.

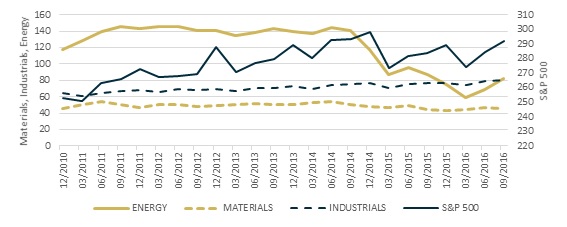

While earnings numbers are driven by many one-offs and cost adjustments, the revenue numbers are more indicative of what the current state of the economy is. S&P 500 sales are still to recover to the 2014 levels. Large part of the recovery is due to the rebounding oil and materials prices; however, revenues of the energy sector are still down 42% since the peak a few years ago. Materials sector revenues are down 17% and given their combined effect on the industrials sector is large enough to limit growth there, the lacklustre revenue performance of S&P 500 since 2014 is no surprise.

Read the complete paper and download tools after registration…

Read the full paper and download tools:

- Buy-and-hold and risk-adjusted return forecasts for 16 key assets over 15 years

- In-depth analysis of trends and their impact on asset returns

- Description of cross-asset pricing methodology

- Sample data spreadsheet for sensitivity analysis – European equities and sovereign bonds

- Historical over- and under-valuation data

![]()

Data Protection Commitment

LINKS Analytics will not distribute your personal data to third parties – no exceptions made. Upon your first request we will remove your data from our database.