“It took me 30 years to understand that returns are calculated incorrectly. It is always assumed that you survive large events.” Nassim Taleb

As events go, economic crises are the big ones. What makes recessions particularly damaging is our misconceptions about them: there is remarkable lack of agreement among economists and investors about the reasons and anatomy of crises. The biggest culprit is of course our inability to differentiate between the cause, the effect and a coincidence.

In this overview, we use our usual toolkit of supply networks and impact transmissions using our in-house system – LINKS Mira. Our starting point was the NBER United States recessions data – a monthly time series since 1854 where 1 stands for recession and 0 stands for no recession. The NBER recession takes account of a number of monthly indicators—such as employment, personal income, and industrial production as well as quarterly GDP growth. In the end, this too is an arbitrary concept, but the best we have to work with. Since data quality and availability prior to the Great Depression are suspect, we begin the study with the 1929-33 events.

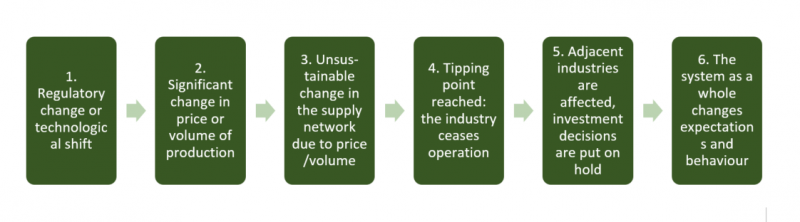

An interesting pattern emerges: all documented crises can be traced back to a significant event that is external to the economic system – usually a major shift in technology (to the extent that technology can be external) or government policy. The external event changes the competitive balance in parts of the supply network. The imbalance grows slowly and after reaching a tipping point where the status quo is not sustainable any longer, explodes and spreads to the adjacent industries.

Network data for recessions

Technology shifts in multiple industries were responsible for the Great Depression, the IT bubble and the sub-prime crisis. But by far the most frequent causes of a recession have been regulatory and geopolitical: cutting government appropriations in 1946, introducing accelerated depreciation in 1954, US oil embargo in 1973 – have all caused significant recessions.

This pattern is remarkably similar to what we have today. A large technological shift in the oil industry – the advent of shale oil, creates a temporary glut in the market forcing oil and other commodity prices to shift. This creates change in behaviour: companies assuming low energy prices in the future invest in energy-intensive technologies. At present we are in the phase of multiple tipping points: shale oil and oil services companies cannot operate because of limited capital and cost issues, petrochemical and utility companies have committed significant resources to oil and gas-related projects and oil majors have cut capital expenditure. In this environment it may only take a minor weather-related change in demand to trigger a another event.

Explore the causes and pathways of all ten recessions here.