The changing environment for growth option pricing in the last decade, namely, higher economic uncertainty and lower cost of innovation, has caused the underperformance of factor portfolios.

Factor portfolios promised to deliver stable and easy-to-predict excess return at no additional risk and relatively low cost – an attractive promise for institutions that are starved for return. Just when the pension funds and endowments successfully built internal capacity for factor investing –the mainstay of quantitative hedge funds in the prior decade or two, the factor portfolios “suddenly” started to underperform the broader markets.

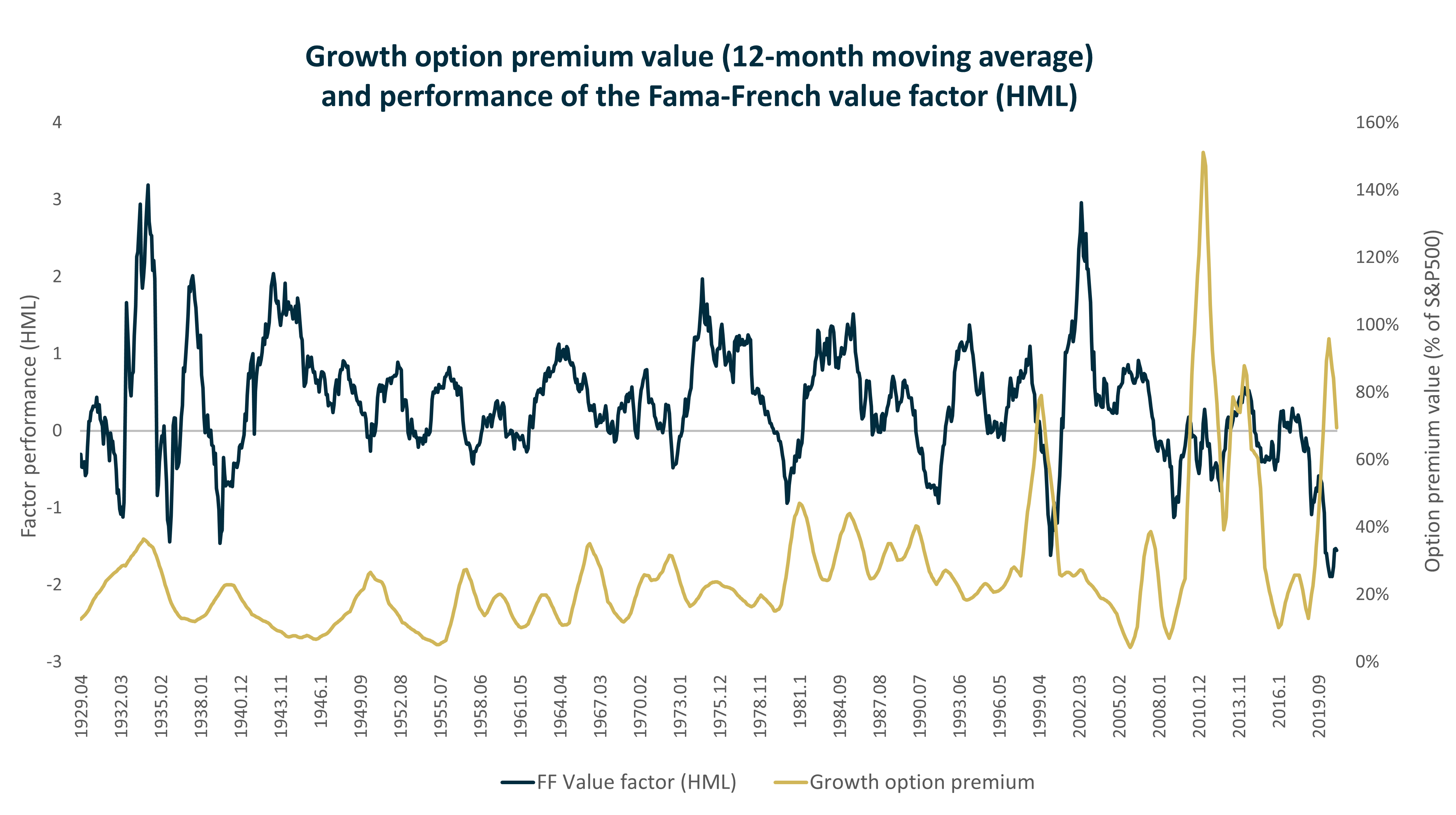

“Factor investing is not about what is included in the portfolio, but rather, about what is excluded from the portfolio – the option value of growth.”

There are of course several “technical” reasons for this underperformance. We rely on several academic studies to examine some of these reasons, including errors, overfitting, crowding out and “fake” diversification. However, the technical reasons are only a part of the story, explaining only up to half of the performance shortfall.

A significantly larger part of the perceived underperformance, in our view, is due to misunderstanding the source of expected returns from factor investing in the first place.