Counterparty Risk: Comprehensive Bank Risk Assessment

Comprehensive

Flexible

Data Sources

Critical and conservative methodology

-

Off-balance sheet exposures have long masked the actual performance of the banks, with most banks using various types of special vehicles (SIV, SPE, VIE etc.) in their securitization programs. All off balance-sheet exposure found in the footnotes, where possible, has been added to total assets.

-

Derivatives exposure has understandably created another layer of risk and complexity. In our assessment we have included a certain proportion of gross reported exposure on balance sheet to reflect the inherent leverage and risk of the position.

-

Apart from counterparty collateral risk, there is a significant fair value model risk for a part of this portfolio that is in the Level 2/3 group – set of assets that are included in the balance sheet at a model-based value.

-

Quality of share capital has been another contentious issue, particularly for the European banks. Tier 1 and Core Tier 1 capital adequacy assessments are too lenient towards banks. We have opted for focusing only on common share capital for the purpose of capital adequacy.

-

SG SOCIETE GENERALE

-

CITI CITIGROUP INC.

-

CS CREDIT SUISSE GROUP LTD

-

UBS UBS AG

-

SS STATE STREET

-

DB DEUTSCHE BANK AKTIENGESELLSCHAFT

-

BONY BNY MELLON

-

UNIC UNICREDIT, SOCIETA PER AZIONI

- MS MORGAN STANLEY

- GS GOLDMAN SACHS

- JPM JPMORGAN CHASE & CO.

- ING ING BANK N.V.

- CA CREDIT AGRICOLE SA

- BOFA BANK OF AMERICA CORPORATION

- BARC BARCLAYS BANK PLC

- NTRS NORTHERN TRUST CORPORATION

- BNP BNP PARIBAS

- HSBC HSBC BANK PLC

- NORD NORDEA BANK AB

- RBS THE ROYAL BANK OF SCOTLAND PUBLIC LIMITED COMPANY

- SAN BANCO SANTANDER, S.A.

- STNCH STANDARD CHARTERED BANK

- WELLS WELLS FARGO & COMPANY

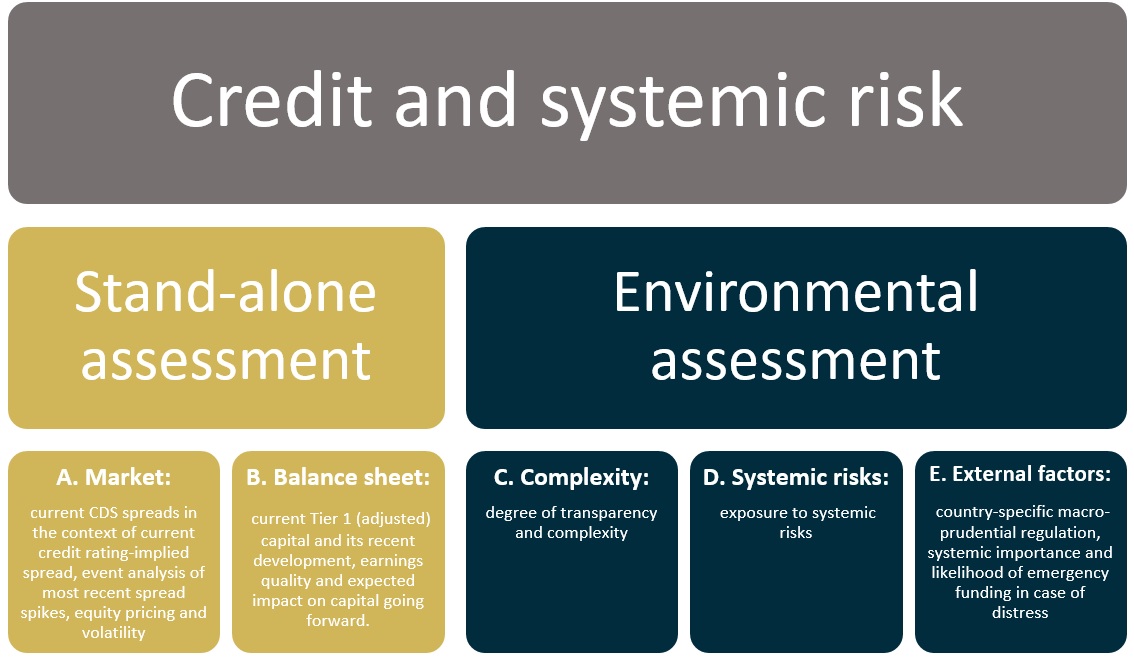

Rating of Major Counterparty Bank

All major counterparty banks are rated based on the five pillars of risk. A comprehensive coverage of all risk factors including:

-

Rating-implied CDS spread premium

-

Equity realized vs. VIX-implied volatility

-

Degree of complexity, including (Level 1/ Level 2,3 assets)

-

Exposure to systemic risks

-

Sustainability of home-base country finances

Sample Spreadsheet: Deutsche Bank

Request your

Commitment-free Trial

Please leave us your email and we will be in touch instantly with information on our pricing options range: from off-the-shelf cost-efficient subscription to additional in-depth research needs.

What our client say

“The fact that your model (MIRA) has a different methodology/approach than the standard stochastic ALM model, resulting in a different view of the world, definitely gives food for thought. In our previous ALM-study we used the standard model, but we were not very enthusiastic about that, as it did not add much value but was more of a confirmation of our assumptions. Your approach is absolutely more challenging and that is exactly what we are looking for. What also helps us a lot is LINKS analysis of the differences of underlying assumptions/views of the world, specifically the requirements that need to happen in order to “accept” our core assumptions.”

Head of Investments, major pension fund (over 30 billion AUM)

“This (Mira) is exactly what we would have developed internally if we had the time and resources. It helps to price assets consistently and does not ignore the underlying complexities. The fact that it also handles liabilities and is flexible enough to incorporate various pricing models for different asset classes is a big plus”

Head of Strategy, major pension asset manager (over 50 billion AUM)

LINKS Risk Severity Review

Leave us your email address and we will update you periodically on major global investment risks covered by LINKS and their severity.