Macroeconomic theories do not determine prices. Companies and individuals do. We examine several theories supporting a regime change towards a higher inflation environment in the long-term and find all of them lacking evidence from the ground. We then propose firm-level reasons for persistent inflation and highlight indicators that could point at the direction of prices in various industries going forward.

- There is little doubt that a combination of lower capacity utilisation due to Covid-19, higher income due to the fiscal stimulus in the US and temporary shift in the consumption patterns away from services and into food and products triggered the first bout of inflation starting with food prices in April 2020. The war in Ukraine has added more pressure on energy and food prices in 2022.

- Capacity utilisation and the supply chain functioning have nearly recovered to the normal levels, and the spending patterns have returned to the pre-Covid structure. However inflation levels persist, prompting the need for more long-term explanations, among them the demographics (shortage of labour), wage-price spiral, raw materials (resource) limitation theory and de-globalisation.

- Upon closer look, neither of these explanations for long-term inflation is supported by data, at least for now.

- Looking at the firm level, persistent inflation can be explained by the combination of a very large disruption due to Covid and the very slow repricing reaction by companies that often takes up to 18 months or longer.

- The key to the question of whether the price hikes will continue lies in the volume response by consumers: large volume declines would mean that it may be more optimal for firms to cut prices. There is significant evidence of volume declines across food, transport, housing and recreation industries, suggesting that at least in some of these industries, price cuts are likely to be the norm going forward.

- Although record high local energy prices in Europe due to the war in Ukraine may add additional inflationary pressures, energy intensive industries in Europe still enjoy very high margins and it will be suboptimal for them to continue increasing prices in the face of falling volumes. An additional limiting factor will be the “imported deflation/stabilisation” from the US.

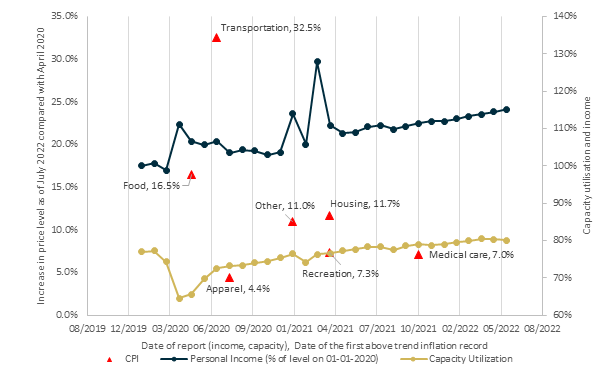

Figure 1: Capacity utilisation, personal income (% of the level in January 2020) and Consumer Price Index component change from the date of the first above trend level to June 2022. Source: US BLS, FRED, LINKS calculations