Institutional investors increasingly notice that the results of an ALM study become irrelevant almost immediately or shortly after the ALM exercise. Why is that?

Traditional statistical models use historical relationships to create future scenarios. If there are no comparable historical precedents (think of Brexit, Covid-19, demographic developments, blockchain, etc.), a future scenario based on an extrapolation of the statistical past, however intelligent, becomes nothing more than a guess. It is therefore not surprising that most of you have had the frustrating experience of ALM results not being very realistic or useful. Yet you continue working with them, having no other viable alternative.

It is not an ideal situation and that is why we – Triple A – Risk Finance in collaboration with LINKS Analytics, have worked on a solution to achieve a better ALM process.

“BpfBOUW has been using deterministic scenarios in the ALM studies for years to map out the consequences of various possible developments. In the “traditional” approach to ALM studies, long-term equilibrium values are assumed based on historical averages and relationships. Various probability calculations then follow from the stochastic analysis and, of course, sensitivity analysis can also be performed on specific variables. The question, however, is whether and to what extent historical averages can be applied to the future. It therefore helps us enormously to gain insight into the outcomes of specific integrated scenarios that we consider plausible and / or regard as high risk. A well-founded and consistent “storyline” of those scenarios helps to better understand the outcomes and sensitivities.” – Linda Teer, Manager Investments, bpfBOUW

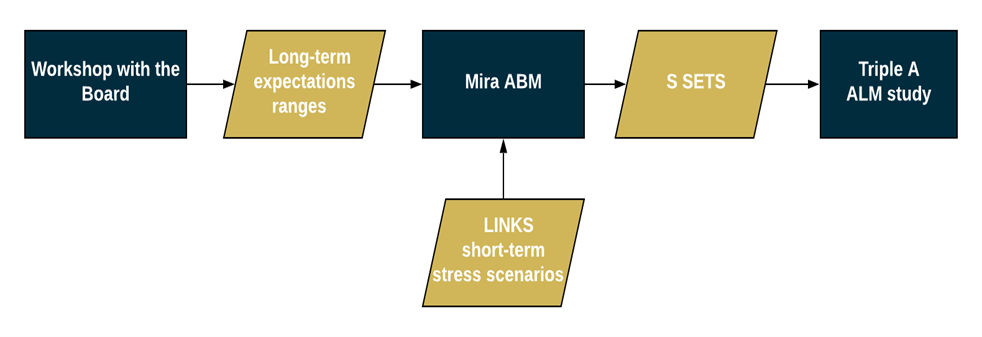

LINKS and Triple-A provide all the required supporting information for the Board to form and articulated the scenario inputs during the workshop. At the end of the workshop the fund will have defined the reasonable inputs for the scenarios. Following the workshop, fully worked out return expectations – Scenario Sets are introduced to the Board.

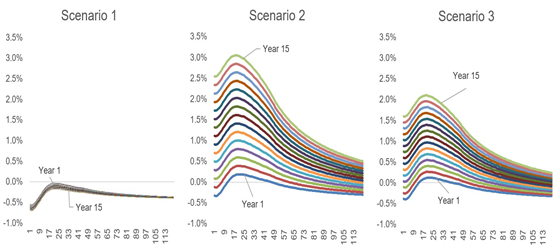

The Scenario Sets contain the full development of the average expected return per year for all investment categories and the yield curves for discounting the liabilities under different scenarios.

LINKS Analytics and Triple A – Risk Finance help pension funds and insurers conduct consistent scenario-based ALM studies.

LINKS Mira ABM is a strategic risk and return management tool that translates world views into consistent scenarios. Mira ABM is fully integrated with the ALM model of Triple A – Risk Finance, whereby scenario triggers and policy sets are included in the assessment as standard. With this integration, the scenario-based ALM management process can be successfully implemented.