As the recent Deutsche Bank episode illustrates, counterparty risk management for pension funds and insurance companies should be based on more proactive and comprehensive assessment of all risks relating to the counterparty. Many Boards and investment committees, undoubtedly, have revisited their exposure to Deutsche Bank at some point during the episode and have had to make a quick decision (one way or another) based on limited amount of information. Such a decision would have been made easier with information beyond credit ratings, CDS spreads and rumours.

The situation is of course more complex than a few numbers can suggest: on the one hand, most major counterparty banks have extremely complex balance sheets, with off-balance-sheet exposures significantly more important than what is on the balance sheet. Based on our assessment of major counterparty banks, on the average, assets recorded on the balance sheet are only 65% of all assets that can be traced to the banks. This is possible through the use of special vehicles (SIV, SPE, VIE etc.). Furthermore, due to the so-called Master Netting Agreements, only a small proportion (~ 0.05%) of the total notional value of derivatives is actually included in the balance sheet. All of this creates huge uncertainty, which is not resolved by the politicized and commercial nature of credit ratings.

On the other hand, many banks, and not least Deutsche Bank, constitute a systemically important part of the global financial flows and as such will not only attract greater scrutiny from the regulators but also greater willingness to bail out in case of distress. Certainly the ability and willingness of the government to bail out banks has an implication for the credit risk. But not all home-governments are equally well-off to be able to afford such a rescue. So how does one reconcile all of these factors when dynamically assessing limits to counterparty exposures? Just how risky was the Deutsche Bank episode and what can be done to manage the risks in the future?

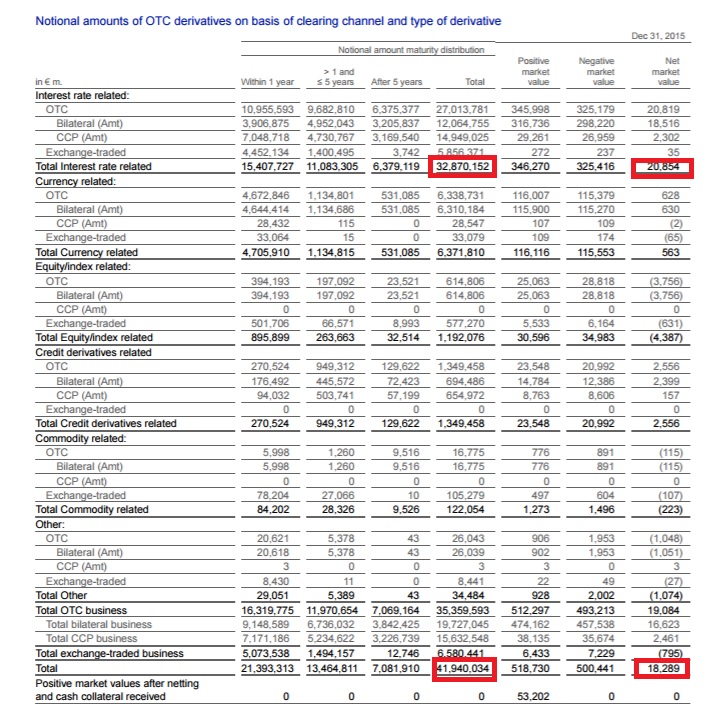

To take the example of Deutsche Bank, assessing the extent of the risk as the news flow arrived would have been easier with the insight of what is not on the bank’s balance sheet. Along with all the other major investment banks, Deutsche Bank has a significant derivatives exposure. Based on their 2015 annual report, the notional value of these derivatives is a little below Eur 42 trillion. Large part of this exposure (Eur 32.9 trillion) is in interest rate swaps. To be clear, the bank’s economic exposure is a fraction of this value – only about Eur 20 billion, or about 0.06%. A non-event then?

Not quite. The intricate mechanism of cash (or equivalent) collateral is in place to manage the counterparty risk of all the parties involved. One side of a trade in such a case is usually a pension fund or insurance company hedging its liabilities, while the other side – a hedge fund or bank. When for whatever reason there is distress in the market, such as the one we saw for Deutsche Bank (DB), trades that are unwound in one direction (in case of DB reportedly by a number of hedge funds) are likely to create quite a bit larger open exposure. What is more troubling, if interest rates begin to climb, as they do in these circumstances, there will be a large need for cash collateral from the side that gains, while the side that loses might fail to deliver the required collateral, thus exposing DB.

Judging by unaffected EONIA and LIBOR spreads, however, there is still little cause for panic. A number of factors help mitigate the specific risk. First, Deutsche Bank happens to be in the second group of G-SIB banks (Global Systemically Important Banks), a list that explicitly flags to the governments which banks cannot be left to sort themselves out. Second, the sustainability gap of Germany’s debt is a positive 1.5% (source: LINKS Counterparty Risk Assessment) – one of the few governments able to arrest any negative development, although the size of the (hypothetical) rescue is a whopping 5.3% of GDP.

Having these numbers at hand makes discussion on active management of counterparty risks more tangible and productive; as always, being prepared is the first line of defence.